Today February 26, 2026, 02:24 PM

Today February 26, 2026, 02:24 PM

It’s fairly remarkable that, for all the economic challenges that California life can produce – plus a rocky economy in 2025 – Golden Staters still pay bills better than their fellow Americans.

That includes Texans and Floridians.

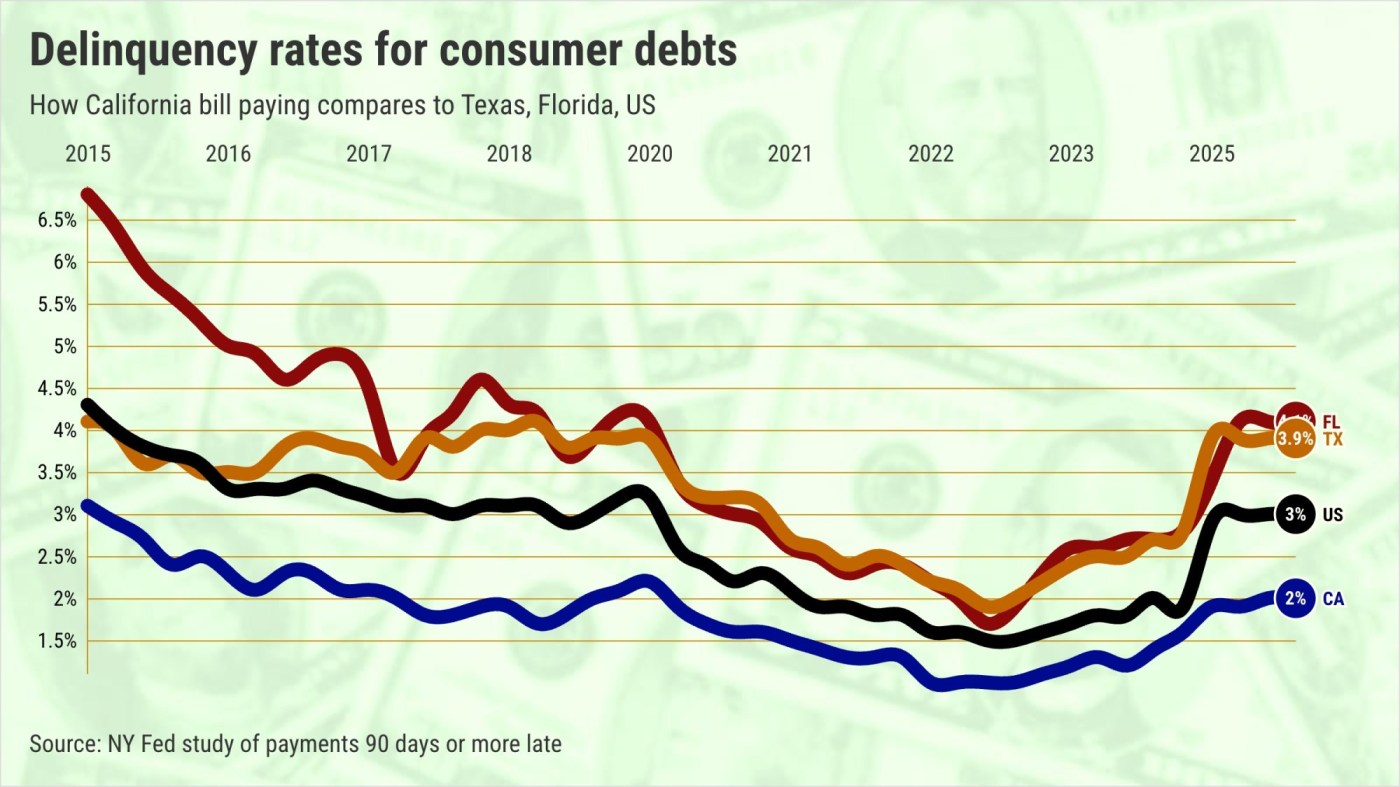

One way to track consumer financial stress is eyeballing the New York Fed’s quarterly analysis of who’s paying their bills on time. These figures are compiled from credit histories from Equifax. So, we’re talking about bill-paying patterns of folks with credit profiles.

The New York Fed report shows that 1.9% of California consumer debt was, on average, 90 days or more past due for all of 2025. My trusty spreadsheet found that this is much better than the 3% of delinquent consumer debt nationwide. For California’s two main economic rivals, Texas and Florida, tardiness was 3.9%.

However, one trend is fairly universal: skipped bills rose last year. However, please note that delinquency rates in much of the nation are running below what was witnessed during the pre-pandemic period of 2015 through 2019. Or what some call “the good ol’ days.”

This trend suggests that recent economic struggles, statewide and nationally, are having a modest yet noteworthy impact on the finances of everyday people.

Think about California’s 2025 tardiness. Delinquencies are up from 1.4% in 2024 but remain below the 2.2% slow-pay rate of 2015-19.

It’s the same nationally: Last year saw a delinquency boost from the 1.9% tardiness of 2024, but below the 3.3% rate of 2015-19.

Florida was much the same. Skipped bills increased from 2.7% in 2024 but remained below the 4.8% level of 2015-19.

However, the late payment rate in Texas increased from 2.6% in 2024 and exceeded the 3.8% rate observed during 2015-19.

How can this be?

We often forget California’s secret sauce: by most broad measurements of income, Golden State paychecks are relatively hefty.

Ponder per-capita income for 2025’s third quarter. California was at $90,400, fourth-highest among the states, according to Bureau of Economic Analysis estimates. That was up 41% from the pre-pandemic 2019 level, the 11th-largest increase among the states.

Nationally, this yardstick of income was $76,500 – that’s 15% less than in California. U.S. incomes rose 37% from 2019.

Texas was at $72,600, No. 27 among the states and 20% below California. That’s up 36% from 2019, the 16th smallest gain.

And Florida was at $75,60 – 19th highest and 16% below California. Six-year growth was 41%, the 14th-best.

Californians do have large debts – mostly because of the huge mortgages attached to the Golden State’s expensive houses.

But California consumers have cooled their borrowing compared to other Americans.

The Golden State’s $87,800 per-person debt last year was up 2% from 2024 and represented a 27% increase since 2015-19.

Yes, last year’s $63,200 U.S. personal debt load was 30% lower than that of Californians. Yet, this nationwide burden increased by 3% over the past year and is 30% above the 2015-19 average.

In Texas, the $59,900 per-person debt last year was up 4% from 2024 and 46% above the 2015-19 average. And Florida’s $62,200 debt in 2025 increased by 3% in 2024 and was 44% above 2015-19 levels.

How big are Golden State home loans?

By this math, there’s $71,600 in mortgage debt per person backing California’s pricey housing.

That’s 55% more than the $46,300 national norm, 78% larger than $40,300 in Texas, and 62% above Florida’s $44,300.

Despite California’s mammoth mortgage debts, these loans are paid on time more frequently than elsewhere in the U.S.

Only 0.5% of California home loans were delinquent last year. Yes, it’s up from 0.4% in 2024. But it’s also below the 0.8% tardiness of 2015-19.

Growing mortgage-payment problems were a national trend, too: 0.9% of American mortgages were delinquent last year. That’s up from 0.6% in 2024, but less than 1.6% pace of 2015-19.

The Texas 0.9% delinquent rate last year was higher than 0.7% in 2024 but lower than 1% in 2015-19.

And in Florida, 2025’s 1.5% late-pay rate was up from 1% in 2024 but below 2.7% in 2015-19.

Contemplate another measurement of bill-paying skill: credit scores derived from consumers’ bill-paying history.

Again, Californians have debt-management prowess.

The average Californian had a score of 723 last year, according to the credit tracker Experian. That’s up from 708 in 2019.

The typical American had a credit score of 715 in 2025, an improvement from 703 in 2019.

These grades fall within what is considered a “good” range of credit-handling histories on a scale that goes as high as 850.

California’s rivals didn’t look so hot. Texans averaged 695 scores last year vs. 680 in 2019. And Floridians? 707 vs. 693.